Performance Update

Global stock markets fell last month, with the FTSE 100 and S&P 500 falling -4.75% and -2.66% respectively. Gilts and Gold also fell. With most asset classes falling our portfolios fell between -1.42% and -2.50%.

As we write, we don’t know the result of the US election. We do know that stock markets will be volatile over the next few weeks as they react to whether Trump or Biden win. Biden is likely to print more money but also raise taxes. Trump will continue on his aggressive foreign policy, but maintain taxes at a lower rate. It is difficult to know how markets will react to each outcome.

The UK has now joined France, Germany, Belgium and Greece in a national lockdown and this is one of the main reasons stock markets fell in October.

We must remember that stock markets are more worried about the longer term earnings of companies rather than what is happening in the short-term. We must also remember that the most heavily affected sectors, namely the hospitality sector, do not make up a significant part of the major stock market indices. We saw this during the first lockdown during which technology companies rose significantly and this caused stock markets to recover after the initial crash.

Perhaps the most important factor that will affect stock markets over the next month will be the amount of fiscal stimulus that US politicians will agree on. They have been arguing over the next fiscal stimulus (their equivalent of furlough and more) and due to the election, nothing was agreed.

We must also remain mindful of what will happen after this lockdown and how a vaccine, improved test and tracing as well as the notion of herd immunity will affect stock markets. We know a vaccine is imminent, we just don’t know how effective it will be (if at all). This news will undoubtedly be the most important for stock markets.

The performance of the portfolios over the last month, 6 months and 1 year is shown below:

| Portfolio | 1 month (Performance %) | 6 months (Performance %) | 1 year (Performance %) |

|---|---|---|---|

| Retirement Investment Solution 1 | -1.42 | 2.62 | 0.50 |

| Retirement Investment Solution 2 | -1.70 | 2.92 | 0.49 |

| Retirement Investment Solution 3 | -1.97 | 3.24 | 0.49 |

| Retirement Investment Solution 4 | -2.23 | 3.55 | 0.48 |

| Retirement Investment Solution 5 | -2.50 | 3.86 | 0.46 |

Trend Following Signals

The table below shows whether the asset class is either in a positive trend (✔) or a negative trend (x). The portfolios will have more exposure to those asset classes in a positive trend and less (if any) to those in a negative trend. These are the main asset classes we monitor:

| Asset Class | Trend Signal | Trend Signal | |

|---|---|---|---|

| Global Equity | ✔ | Emerging Market Equity | ✔ |

| UK Equity | ❌ | Commodities | ✔ |

| Europe ex UK Equity | ✔ | UK Corporate Bonds | ✔ |

| US Equity | ✔ | UK Corporate Bonds (Short dated) | ✔ |

| Japan Equity | ✔ | UK Index Linked Bonds | ✔ |

| Pacific Equity | ❌ | Global Bonds | ✔ |

| Gold | ✔ | UK Gilts | ✔ |

| Global Property | ❌ | Emerging Market Bonds | ✔ |

| Global Infrastructure | ❌ | Overseas Corporate Bonds | ✔ |

Smart Equity” Exposure

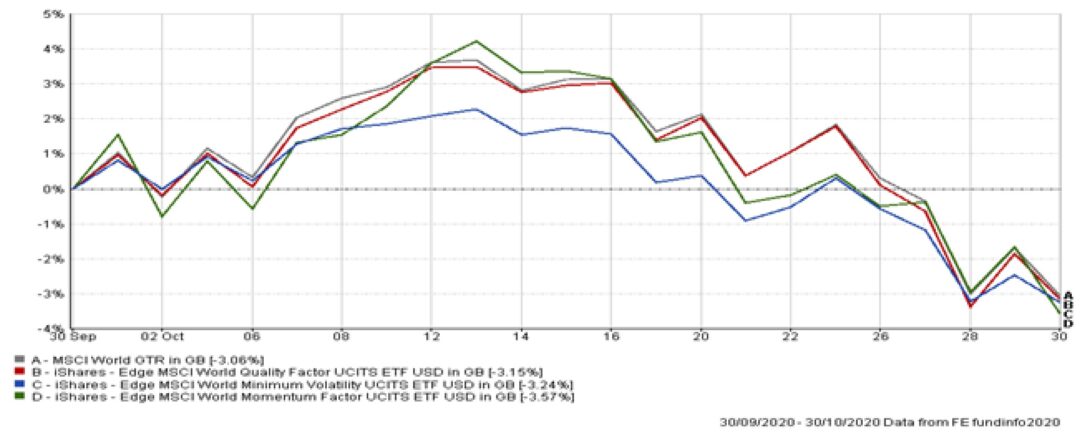

Academic research has shown that if you follow a systematic method for investing, you will significantly outperform against the benchmark. For example, research by the Cass Business School has shown that if you combine a number of “Smart Equity” ETFs in the US market you can beat the S&P500 by at least 1.5% per annum. Our Retirement Investment Solution 2, 3, 4 and 5 portfolios combine Trend Following with “Smart Equity” exposure and invest in three ETFs from iShares which use “Momentum”, Quality” and “Volatility” in an attempt to outperform. For the first time since we launched, they all underperformed (albeit slightly).

Summary of Portfolios

While we continue to see much bad news in the press, with virus cases rising across Europe and a second lockdown in the UK, we must remember that stock markets are forward-looking and they price in the earnings of companies many years from now. We have a huge pent-up demand from consumers whom have been saving their income, low interest rates and further Government spending to come. Therefore, when we have controlled the virus, we expect a surge in spending and thus increased profits within many of the companies we invest in.

Herd Immunity

As we enter a second national lockdown, the news is full of rising infection rates and unlike the lockdown in March, the rain and winter is here. It is understandingly easy to be negative.

However, there are also some interesting opinions that we are very close to the end of this pandemic that are not receiving coverage in the main press. It is certainly worth looking at these opinions. At this stage we must point out that we are not virologists and cannot provide any further evidence as to the validity of these opinions, but if they are indeed true, then we have the catalyst for stock markets to move much higher.

The first opinion to look at is the “Great Barrington Declaration”, which was signed on the 4th October. This is a proposal drafted by experts in the field of epidemiology and the basic principle is that the current lockdown policies are producing significantly more harmful effects on health (less people vaccinate their children, go to cancer screenings, more suffer from mental health, etc). This will cause greater excess deaths in the long-term. Their principle is that we should let the virus pass through those parts of society who have minimal risk of death, until we eventually reach herd immunity. The World Health Organisation believes that this strategy is dangerous.

The second opinion that is certainly worth investing an hour of your time in, can be watched via a video by Dr Mike Yeadon. If you search his name and buzzsprout then you will find the podcast, or you can simply use this link:

https://escapefromlockdown.buzzsprout.com/1013854/5745529-episode-21-dr-mike-yeadon

The essence of his argument is that SAGE, the governments scientific advisory body, has assumed that there is no prior immunity to Covid-19, whereas his belief is that 20-50% of the population has immunity to the virus via T-cells. This is backed up by some existing research on previous viruses. If this is true, then we are much closer to herd immunity and the end of the virus. He also believes that the statistics being presented to the government, including the amount of false positive results in the current Covid tests, are wrongly influencing our reactions to the virus.

Finally, the British Medical Journal has published a peer reviewed article that discusses herd immunity in a much more scientific way. This is quite a hard read, but interesting:

https://www.bmj.com/content/370/bmj.m3563

The article discusses the need to do more research on pre-existing immunity and how we could be close to herd immunity without a vaccine.

Summary

We are not scientific experts and cannot verify whether these opinions are correct but it is certainly interesting to be aware of them. Stock markets have somewhat recovered from the crash in March and they are telling us that we are close to the end of the virus that is causing so much disruption to the global economy. Stock markets are forward looking and therefore more concerned about the future earnings of companies in a year’s time, rather than today. If we are indeed closer to herd immunity than the mainstream press believe, then the global economy will pick up much more quickly than expected and stock markets will almost certainly experience a strong move higher.