With Labour now in office, tax reforms are expected to focus on wealth taxation and incentivising business investment.

Labour is making as much political capital over the “discovery” of a £22 bn black hole in the public finances, but is this real or just political game-playing? During Prime Minister’s Questions in May 2024, Labour leader Keir Starmer questioned Conservative Prime Minister Rishi Sunak about the alleged £46 billion black hole in the government’s finances. So, judge for yourself.

There have been disputes over the accuracy of the £46 billion figure, with some experts arguing that it is an exaggeration or based on flawed assumptions. The Conservative government maintained that the black hole is a result of Labour’s planned spending increases, which would put pressure on the public finances.

However, the message is very clear is that Labour is laying the ground to raise taxes, and it’s causing some of our clients some anxiety. So we’ve produced this rather lengthy article to consider what leading experts think will be the most likely changes, and which taxes are unlikely to materially change.

Here’s an overview of the likely changes, based on expert analysis and sources.

1. Capital Gains Tax (CGT)

Labour has not confirmed any immediate changes to CGT rates, but tax experts anticipate increases. The potential for CGT to align with income tax rates, with a top rate of 45%, is a significant possibility. This would mark a sharp rise from the current rates of 20% for most gains and 28% for residential property gains. While popular reliefs like the Principal Private Residence Relief (PPRR) are likely to remain, Labour could remove the CGT uplift on death. Currently, this allows beneficiaries to inherit assets at their market value without paying tax on gains made during the original owner’s lifetime. Removing this uplift would likely increase the tax burden on inherited assets [1][2].

2. Income Tax

Labour has committed to maintaining current income tax rates, but reforms to the personal allowance taper are anticipated. At present, individuals earning over £100,000 see their personal allowance gradually reduced. A likely change would be reducing the income threshold (to £70,000?) at which this taper begins, leading to a higher effective tax rate for those on higher incomes. Advisors should help clients assess the impact this might have on their net incomes and look for ways to optimise tax reliefs [3].

3. Inheritance Tax (IHT)

Labour’s IHT reforms are expected to focus on restricting reliefs like Agricultural Property Relief (APR) and Business Property Relief (BPR). These reliefs allow individuals to reduce or eliminate IHT on certain agricultural and business assets. Labour’s potential focus will be on tightening these reliefs, especially for non-farming landowners, to ensure that they are only available to those actively engaged in farming or business [2][4].

Additionally, Labour might reduce the IHT threshold, currently set at £325,000, or limit the residence nil-rate band for passing on the family home tax-free. These changes could push more middle-class families above the IHT threshold due to rising property values [3].

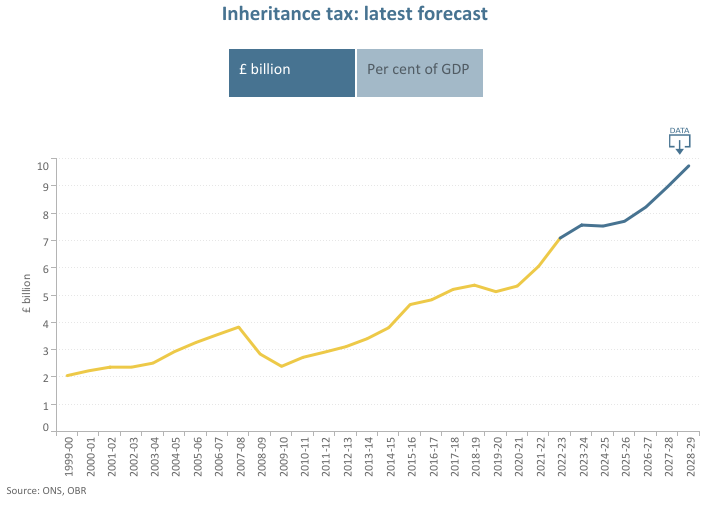

Leading tax experts believe that IHT changes will be symbolic rather than meaningful: Without making any changes, the revenue raised from this tax is forecast by the OBR to rise from £7.1 bn to £10 bn annually by the end of the decade.

IHT is a complex tax to reform with impacts on many other legal arrangements such as trusts, and so a major reform would need to be root and branch and take several years to pass through Parliament.

4. Business Relief and Innovation Investment: EIS and VCT

Key to Labour’s plans for fostering innovation and business growth are the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT), which offer significant tax reliefs to investors. These schemes are set to expire in 2025, but Labour is expected to renew them. EIS and VCT provide income tax relief of 30% for investors in early-stage, high-risk businesses, along with CGT deferrals and exemptions on gains from qualifying investments [5][6].

These schemes have been crucial in driving almost £7 bn [8] investment into technology, biotech, and green energy sectors, and Labour’s renewal would signal continued support for entrepreneurship and innovation [6].

5. Non-Domicile (Non-Dom) Tax

Labour is expected to abolish the non-dom tax regime, which currently allows UK residents to avoid UK taxes on foreign income and gains. This would mean all UK residents, regardless of domicile status, would be taxed on their worldwide income and gains. Advisors should review clients’ offshore structures, ensuring they are prepared for this shift [7].

6. Reforming Pension Taxation: Detailed Revenue-Raising Options

The Institute for Fiscal Studies (IFS) [9] suggests several reforms to the UK pension taxation system aimed at raising revenue. Their primary proposal is to restrict higher-rate tax relief on pension contributions to the basic rate, which could raise £15 billion annually but may discourage saving. The IFS advises against reducing the 25% tax-free lump sum for smaller pensions but supports taxing pension wealth via inheritance tax to ensure fairness across wealth groups.

For a more detailed analysis, visit the IFS here.

Final Thoughts

Labour’s tax reforms are likely to focus on redistributing wealth, with changes to CGT, IHT, and non-dom taxes on the horizon. However, there are several strategies that clients should discuss with their financial advisors to mitigate the impact of these reforms:

- Accelerating Asset Sales: Clients should consider selling or gifting assets before potential CGT increases, especially those with significant gains [1][2].

- Estate Planning: With IHT changes likely, particularly around APR and BPR, it’s crucial to review estate plans and ensure that clients’ assets are structured to take advantage of existing reliefs while they remain in place [2][4].

- Investing in EIS and VCT: The potential renewal of these schemes provides an excellent opportunity for tax-efficient investments in innovative sectors. Advisors can help clients explore these schemes to maximise tax relief [5][6].

By planning ahead and maximising current reliefs, clients can reduce their exposure to the tax changes Labour is expected to introduce.

Bibliography

- Evelyn Partners. “Labour’s Capital Gains Tax Plans Explained.” www.evelyn.com. Accessed September 2024.

- Charles Stanley. “Chancellor’s Speech Signals Labour’s Tax Direction – What Might It Mean for IHT and CGT?” www.charles-stanley.co.uk. Accessed September 2024.

- Farrer & Co. “Non-dom Tax – What Changes to Expect from the Labour Government?” www.farrer.co.uk. Accessed September 2024.

- Weightmans. “UK Inheritance Tax Changes Under a New Labour Government.” www.weightmans.com. Accessed September 2024.

- De Pointe Research. “Will Labour Reform Inheritance Tax? Analyzing the Potential for Change Under the Current Government.” www.depointe.co.uk. Accessed September 2024.

- Saffery. “Tax Changes Expected from the Labour Government.” www.saffery.com. Accessed September 2024.

- Womble Bond Dickinson. “Preparing for the Possibility of a Labour Government.” www.womblebonddickinson.com. Accessed September 2024.

- HMRC – Enterprise Investment Scheme (EIS) statistics (2021)

- How should pensions tax relief be reformed, and could it be done in ways that raise revenue? Accessed September 2024.